Basic Bookkeeping for UK Sole Traders: A Starter Guide for Women Entrepreneurs

Here’s a little story you might recognise.

Here’s a little story you might recognise.

Jane had always washed her clothes by hand. One day, she bought a “magical” washing machine that promised to do all the hard work. Excited, she loaded her clothes, poured in soap… and even a jug of water — all into the same compartment. Then she waited. Nothing happened.

Frustrated, Jane assumed the machine was broken. When she called the shop, the assistant asked, “Did you read the manual?” Jane hadn’t. The truth? The machine worked perfectly — she just hadn’t learned how to use it. And that’s exactly what happens in business. Many small business owners do the same with bookkeeping.

If you’re a sole trader trying to make sense of your finances, this guide is for you. Perhaps you’ve been mixing personal and business money, or panicking when the numbers don’t add up. It’s easy to decide it’s “too hard” or “only for accountants,” but just like Jane, you aren’t doing anything wrong — you simply haven’t been shown how the “machine” works.

Here’s the empowering truth: bookkeeping for sole traders doesn’t have to be confusing or stressful. Learn the basics, and it becomes a tool that saves time, brings clarity, and helps you grow your business with confidence.

By the end of this post, you won’t see bookkeeping as a chore — but as your secret weapon for control, freedom, and success.

1 . Bookkeeping Defined Simply

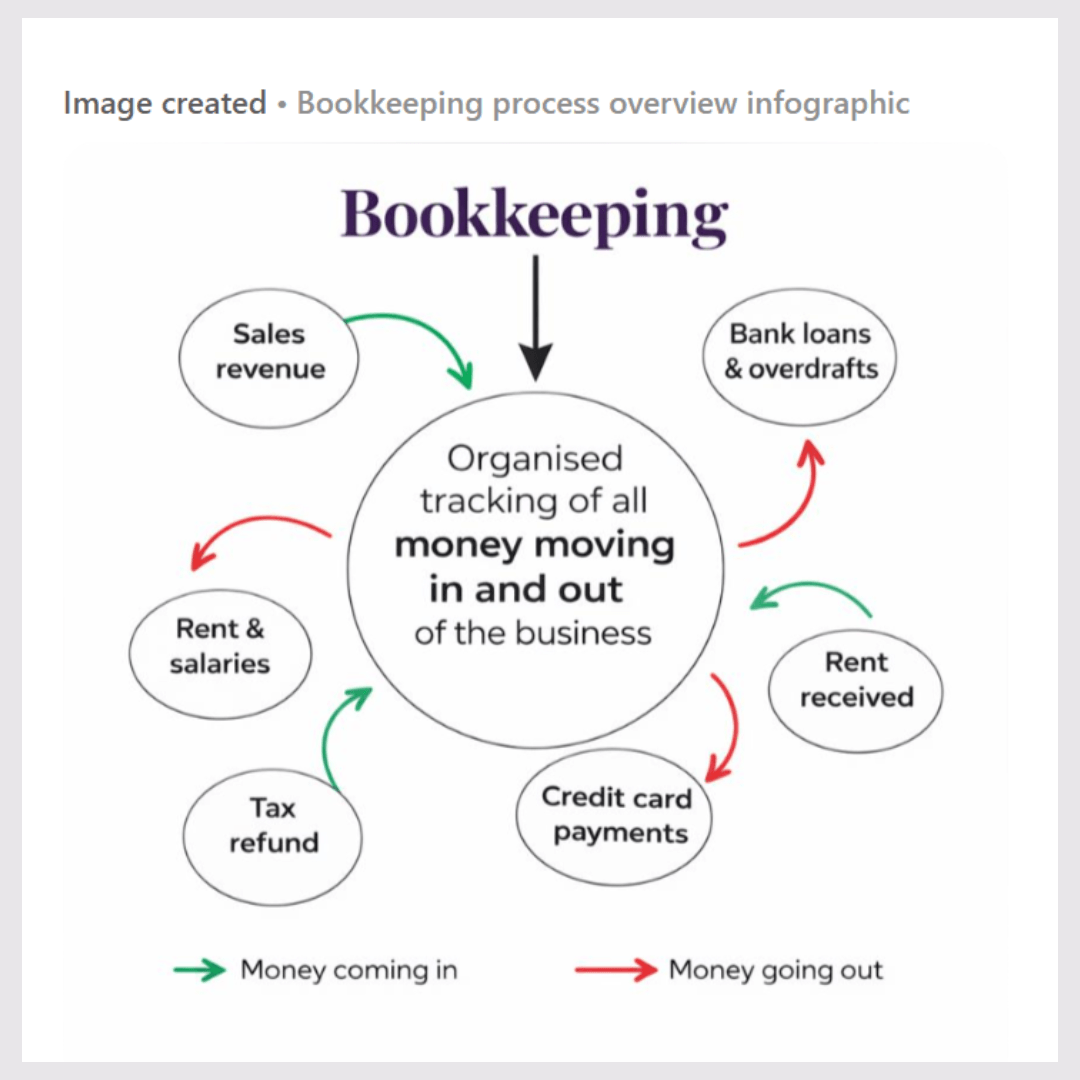

First, let’s get clear on what bookkeeping actually is. Simply put, bookkeeping for sole traders is the organised way of tracking all the money moving in and out of your business.

It helps you clearly see the difference between what you’ve earned (your income), and other money coming in (like loans) or going out (like expenses).

| Money Moving IN | Money Moving OUT |

|---|---|

|

|

Think of it like a daily journal — but instead of jotting down feelings, you jot down numbers. Over time, these records tell the true story of your business finances — not guesses or gut feelings, but facts you can trust.

2. When to Start Tracking Your Transactions

Now that you know what bookkeeping is, you might wonder: “Do I really need to track everything from day one?”

Here’s the deal: in the UK, there’s a trading allowance. If your business earns £1,000 or less in a tax year (6 April – 5 April), you don’t need to declare that income or pay tax.

But if you earn more — or simply want a clear picture of your business — start tracking all transactions as part of simple bookkeeping for sole traders from your very first sale or expense.

Even if you’re under the allowance, keeping records early saves you from the last-minute panic of chasing receipts, filing taxes, or trying to figure out how your business is really doing. Think of it as giving your business a head start — clarity, control, and confidence from day one, instead of stress later on.

3. The Payoff: Why Bookkeeping is Your Ultimate Business Weapon

Now that you know what bookkeeping is and when to start, let’s talk about why it actually matters. Done right, your books aren’t just a record — they’re your ultimate business weapon. Here’s how:

a . Profit Compass: See Clearly, Decide Confidently

Waiting until year-end to see if you’ve made money? That’s like shaking your washing machine mid-cycle to see if it’s working — messy and stressful.

Up-to-date books show your net profit today (that’s the money left after all your expenses are paid), help you spot which products are thriving, and let you pivot fast with confidence.

b. Cash Flow Control: Stop Being Surprised

No more bills or slow months sneaking up on you. Your records show exactly what’s coming in and going out, so you can plan ahead and keep your bank balance healthy.

c. Tax Confidence: Keep More of What You Earn

Lost receipts and missed deductions? That’s money down the drain. Regular bookkeeping ensures you pay only what’s owed and claim every allowable expense. Your books become your audit armour — stress-free proof that you’re compliant.

d. Growth Blueprint: Build Value, Plan for the Future

Thinking of a loan, partner, or even selling your business? Messy spreadsheets don’t inspire confidence. Clean, detailed books show your profits over time and your business’s value, giving you a roadmap for growth.

Put simply: bookkeeping for sole traders isn’t just about keeping records. Done regularly and in a way that makes sense to you, it helps you understand your numbers, stay on top of tax, and make decisions with confidence as your business grows.

4. Unlock Control: The Right Bookkeeping Mindset

Think bookkeeping is just about numbers? Think again.

It’s your secret toolkit — the one that helps you take control, make confident decisions, and steer your business forward without nasty surprises.

Bookkeeping got a bad reputation for a reason. For years, it was treated as tedious, mechanical, and only there to keep the taxman happy. Log the sales, record the expenses, move on.

Let’s flip the script.

For sole traders, bookkeeping is a quiet toolkit — one that helps you take control, make confident decisions, and steer your business forward without nasty surprises.

It’s not just numbers — it’s insight.

Think of it like a map. The more clearly it’s filled in, the easier it is to see where you are, where you’re heading, and how to get there — calmly, confidently, and in control.

5. Your Profit GPS – Mastering the Chart of Accounts (COA)

You’ve seen the power of financial clarity. But how do you turn everyday numbers into decisions that actually move your business forward?

That’s where the Chart of Accounts (COA) comes in.

Think of it as the DNA of your financial story. It organises every transaction into clear, meaningful groups — so your numbers stop being noise and start giving you answers.

A well-designed Chart of Accounts works like a GPS for your profits. It shows where your money comes from, where it goes, and helps you spot problems early — before they turn into stress.

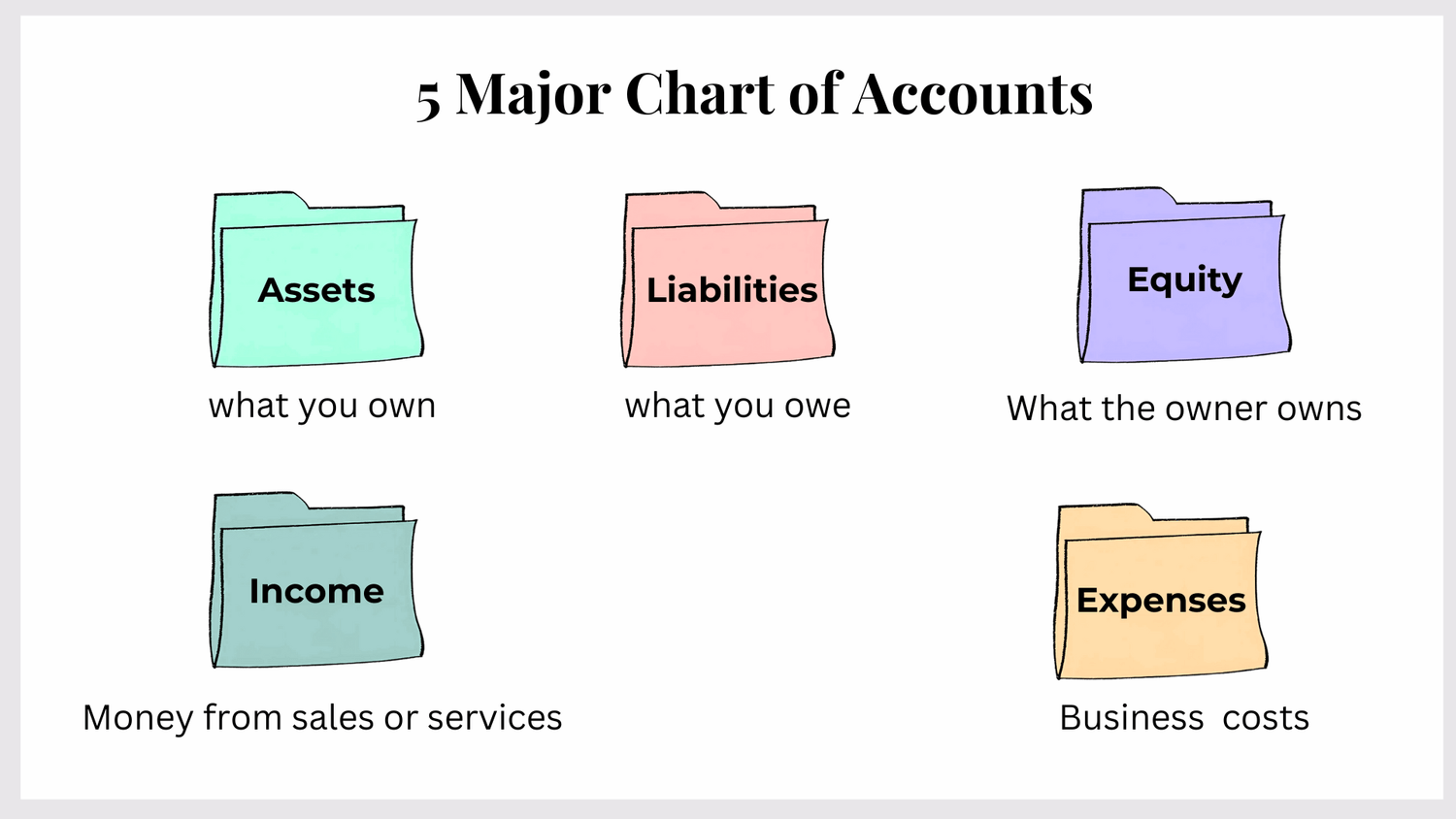

The Five Pillars of Bookkeeping (Inside Your COA)

1. Assets — What Your Business Owns

Assets are things your business owns that have value, such as cash, equipment, or unpaid invoices.

Strategic question:

Am I using what I own to grow — or is it just sitting there?

2. Liabilities — What Your Business Owes

Liabilities are amounts your business needs to pay, such as loans, unpaid bills, or tax owed.

Strategic question:

Am I borrowing to grow — or borrowing to cover gaps?

3. Equity — Your Share of the Business

Equity is what’s left once you subtract what you owe from what you own. It includes your initial investment and profits you’ve kept in the business.

Strategic question:

Should I keep profits as a safety net — or reinvest them to grow?

4. Income— How Money Comes In

Income is the money you earn from sales or services.

Strategic question:

Where does my money really come from, and can I rely on it long term?

5. Expenses — What It Costs to Make Money

Expenses are the costs of running your business, from software and marketing to travel and utilities.

Strategic question:

Am I spending to build my future — or just maintaining habits?

DIY Chart of Account (COA) Power Move: The Naming Strategy

Here’s where most DIY bookkeepers miss a trick: a generic Chart of Accounts hides insight; a strategic Chart of Accounts reveals profit.

When setting up your accounting software, don’t blindly accept the default list. Customise your account names to reflect how your business actually moves money.

Income: Names That Tell the Truth

Most people use names that are too vague, such as:

Sales

Service Income

These tell you that money came in — but not why. Instead, try naming conventions that segment your revenue, like the examples below.

More useful (for a service-based business):

Digital Product Sales — £20,000

Workshop Income — £15,000

General Client Work — £500

Now, when you look at your Profit & Loss report (the summary of what you earned vs. spent), you can instantly see which part of your business is making the most money.

Expenses: Where Clarity Saves Cash

The same principle applies to expenses.

Some people use names that are too vague, such as:

Other Expenses

Instead, create more meaningful expense categories:

Subscription Software — £150

Shipping & Packaging Costs — £100

Marketing Ad Spend — £1,000

Clear names make patterns visible. Patterns lead to better decisions.

When your accounts are named properly, your P&L stops being a historical report and starts becoming a practical tool — one that helps you control costs, protect cash flow, and focus on what actually grows the business.

6. Knowing Your Speed – Choosing Your Accounting Method

Once your Chart of Accounts (COA) is set, there’s one more important choice to make: how you record income and expenses for tax purposes.

In the UK, you must choose one method per tax year and stick with it.

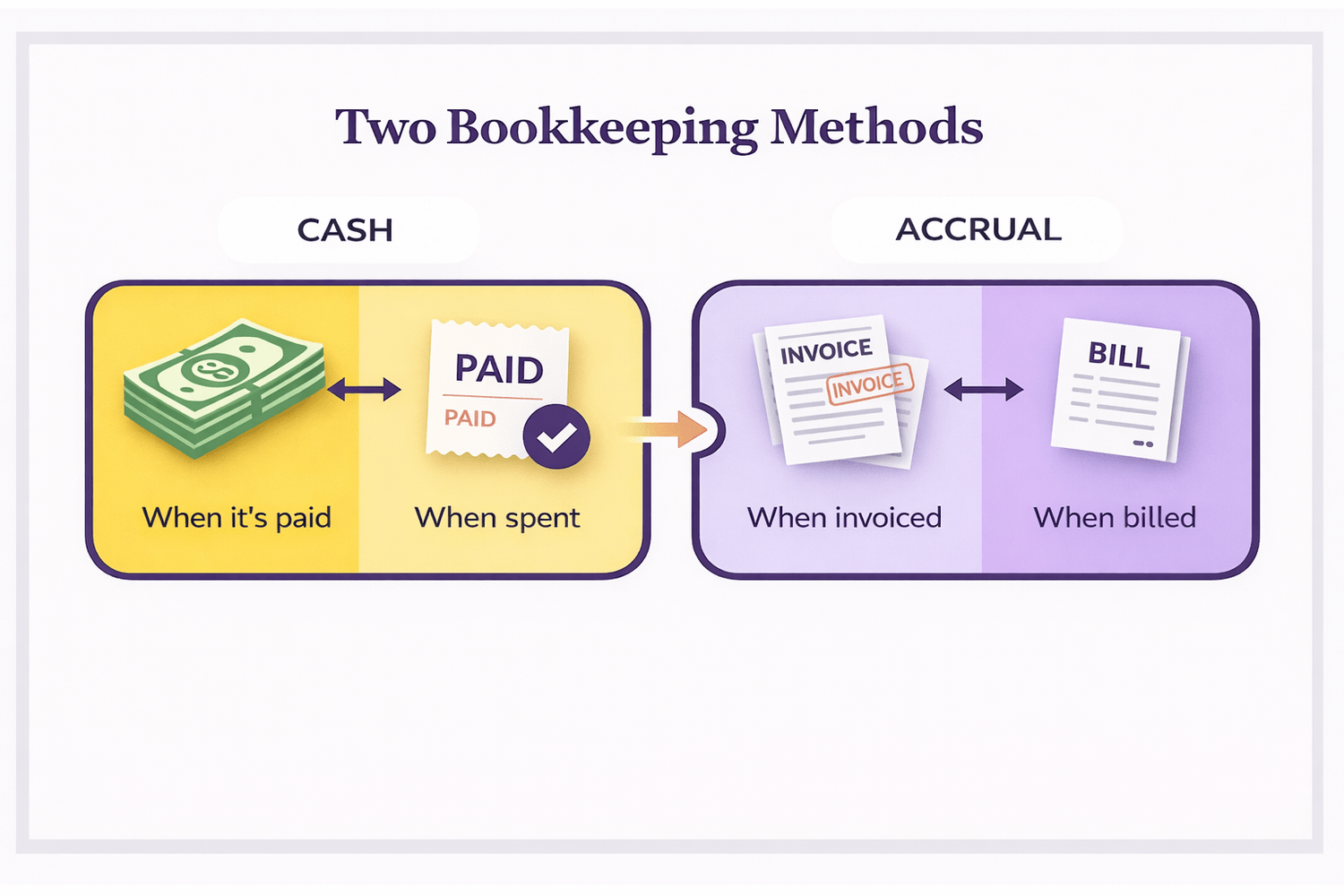

a. Cash Method Accounting – The Real-Time View

With the cash method, you record:

Income when money actually arrives in your bank

Expenses when you actually pay them

Why this works well for DIY bookkeeping:

It’s simple and easy to manage

You never pay tax on money you haven’t received

It gives a clear, real-time view of your cash flow

For many sole traders, this feels the most natural — your records match what’s happening in your bank account. Most sole traders start with cash accounting, and that’s perfectly fine.

b. Accrual Method Accounting – The Bigger Picture

With accrual accounting, you record:

Income when it’s earned (when you send an invoice)

Expenses when they’re incurred (when you receive a bill)

Money doesn’t have to exchange hands for the transaction to count.

Why some businesses choose this method:

It shows your true profit over time

It’s useful if you’re planning to apply for loans, take on partners, or grow

It gives a fuller picture of business performance

Key point to remember

You must use the same method for the entire tax year.

The right choice depends on your business size, how you work, and where you want your business to go next.

7. Choosing How You Record: Single-Entry vs Double-Entry

Before you start logging every sale, “snack break,” and subscription, it helps to understand how transactions are recorded.

Think of these as two recording styles — one light and simple, the other sturdier and more detailed.

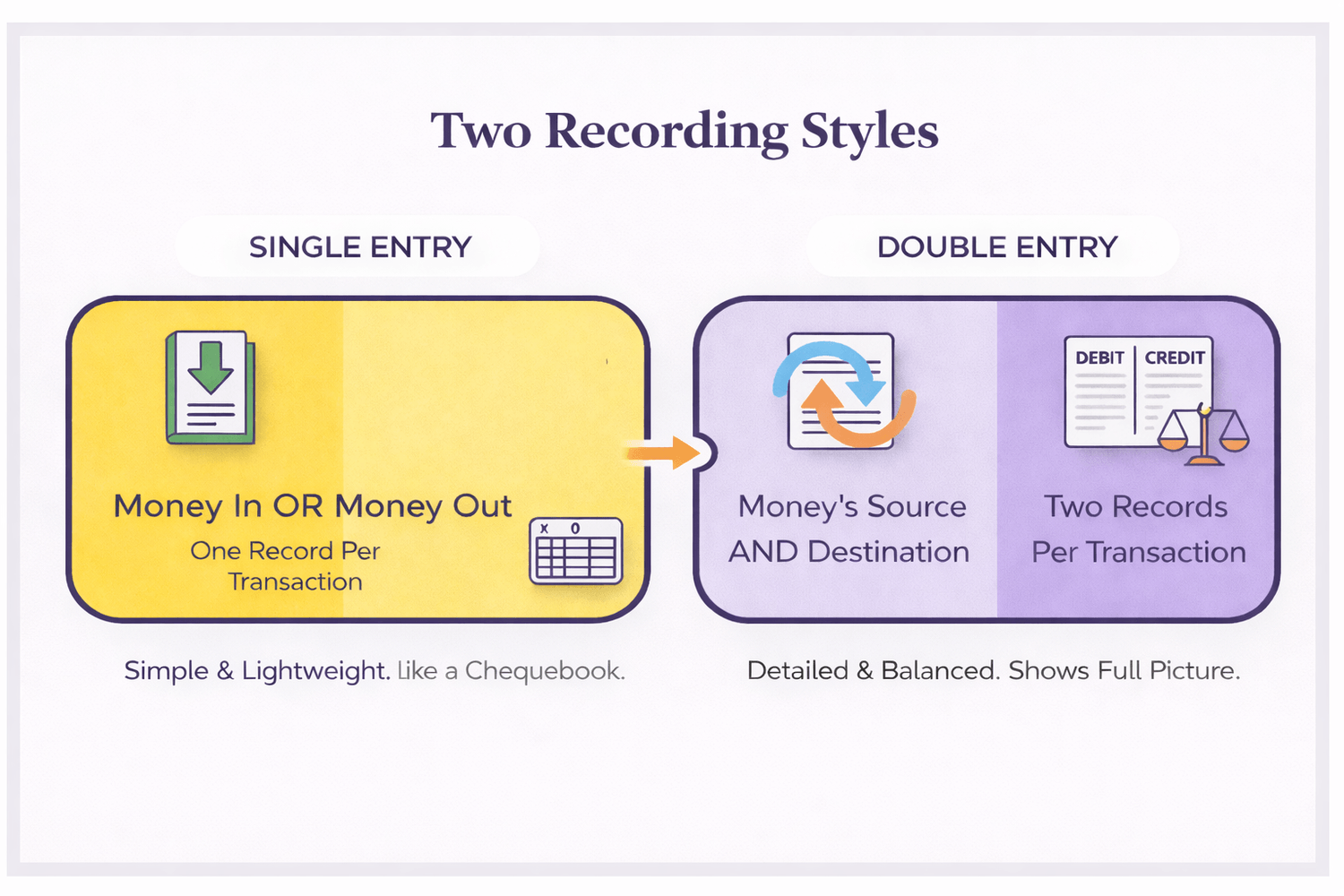

Single-Entry Bookkeeping – Simple & Lightweight

Each transaction is recorded once — money in or money out.

It’s the business version of a chequebook register.

This works well if you’re:

Just starting out

Running a simple setup with few transactions

Double-Entry Bookkeeping – Built for Growth

Every transaction is recorded twice — showing where money came from and where it went.

Best for:

Growing or planning to scale

Managing several accounts

Dealing with higher volumes of transactions

Example: How the Same Sale Is Recorded

You make a £100 digital product sale, and the money is paid into your bank.

Single-entry bookkeeping:

You record £100 in your Digital Product Sales income account (where the money came from).

Double-entry bookkeeping:

You record £100 in your Bank account (where the money went)

and £100 in your Digital Product Sales income account (where the money came from).

This makes it easy to see exactly how much your digital products contribute to your income when using single-entry bookkeeping.

Double-entry adds an extra layer of detail, which becomes invaluable as your transaction volume grows.

If you use bookkeeping software, don’t panic. Double-entry isn’t something you “do” manually. You simply record the sale or expense — the software handles the rest quietly in the background.

8. Choosing Your Tools: The Right Bookkeeping System for Your Business

Today, your bookkeeping system is like your washing machine — the thing that does the heavy lifting for you… as long as you pick the right one.

This section helps you choose the tool that matches your business stage, your confidence level, and your sanity.

And it’s not just about convenience anymore. The way you keep your records now has legal implications too — thanks to a major shift in how HMRC expects businesses to operate.

The Modern Way: Making Tax Digital (MTD)

HMRC is making digital record-keeping the “order of the day.” From April 2026, if you earn over £50,000, you will be legally required to keep digital records and send quarterly updates.

Here are the three main ways to manage your data in this new digital world:

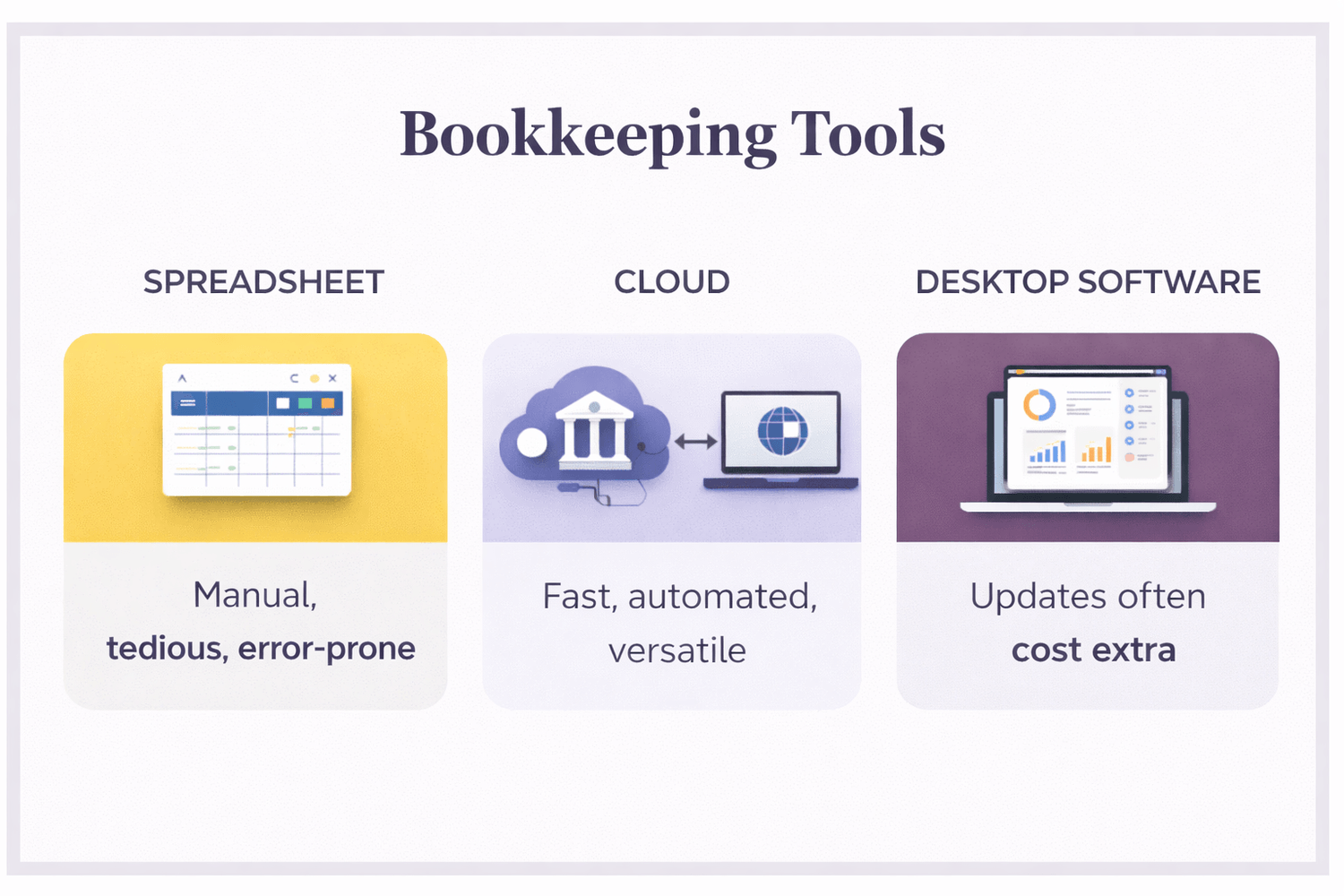

1. Spreadsheets

What it is: Excel or Google Sheets, where you manually type in every sale and expense.

Reality check: Fine for a brand-new hobby — but it’s a “time thief.” It’s easy to make mistakes, and to follow MTD rules, you’ll need extra “bridging software” to link your sheet to HMRC. It’s about as scalable as washing socks one by one in the sink.

2. Desktop Software

What it is: Programs installed on one specific computer (like Sage).

Reality check: It works if you never leave your desk. You’ll still need bridging software to link it to HMRC. Updates often cost extra, and sharing files via email feels very… 2004. Since it’s not in the cloud, you can’t snap receipt photos on the go or let your accountant log in to help you. It’s fine if you don’t need remote access, but it lacks the “anywhere, anytime” ease of newer systems.

3. Cloud Software (Online)

What it is: Apps like Xero, QuickBooks, or FreeAgent that you access via a browser or phone.

Reality check: This is the gold standard. It connects to your bank account to pull in transactions automatically. It’s MTD-ready, allows you to snap photos of receipts, and gives you a real-time view of your profit from anywhere.

The Takeaway

Cloud accounting is the easiest way for modern small businesses to stay compliant. It means less admin, fewer errors, and a much clearer picture of your money.

Three Core Features Your Accounting Software Should Have

Choosing software isn’t about pretty logos. It’s about saving time and stress.

Look for these essentials:

1. Bank Connection & Automation

Your software should securely pull in transactions from your bank.

Why it matters:

No typing, no guessing, no hunting through bank statements like lost treasure.

2. Invoicing & Online Payments

Create professional invoices and let customers pay you online.

Why it matters:

Faster payments, fewer awkward follow-ups, smoother cash flow.

3. Real-Time Reports

Instant access to financial reports like Profit & Loss (income minus expenses).

Why it matters:

You always know how your business is actually doing — no delays, no surprises.

The Three Big Players (UK)

For UK sole traders, these come up again and again:

Xero – Clean, modern, great for creatives and integrations

FreeAgent – Freelancer-friendly, often free with some UK banks

QuickBooks Online (QBO) – Feature-rich, flexible, strong reporting

You can try QBO with a free trial: Try QBO free trial

Full honesty: QBO is my personal favourite and what I use in my own business. It’s intuitive, customisable, and quietly handles the messy bits behind the scenes.

Automation Still Needs Oversight

Jane’s Mistake: The Biggest Software Trap

Remember Jane and the washing machine?

The biggest trap is assuming software categorises everything perfectly on its own.

Automation doesn’t mean zero effort — it means less effort.

You still need to:

Review transactions

Categorise them correctly

Reconcile them with your bank statement each month

Think of it like laundry: the machine does the work, but you still sort the clothes and check they came out clean. A few minutes each month keeps your books accurate and stress-free.

9. Wrap-Up & Empowered Action

You’ve now covered the essentials every sole trader needs to run their books with confidence:

What bookkeeping really is — and why it matters

When to start tracking

The benefits beyond “tax admin”

How to build and name your Chart of Accounts

Accounting methods and recording styles

Choosing the right tools and software

Here’s the heart of it:

Bookkeeping isn’t a chore — it’s your decision-making superpower.

When you understand your numbers, you stop guessing and start steering.

You don’t need to become an accountant. You just need a simple system that works for you… and now you know exactly how to build it.

Your 15-Minute Challenge

Open your accounting software today and give yourself just 15 focused minutes.

Ask yourself:

One small step.

Huge payoff.

Stop Avoiding Your Bookkeeping — Even If You’ve Been Putting It Off

If you keep delaying your bookkeeping or don’t know where to start, this simple guide will help you finally take action — without overwhelm.

👉 Join the Confidence Circle and get practical, supportive guidance to help you feel more confident, consistent, and in control of your finances.

Share This Knowledge

If this post helped you feel more confident about your bookkeeping (or saved you a headache), chances are another business owner needs it too.

Feel free to share it using the links below — because clarity is even better when it’s passed on.

Explore More Resources to Empower Your Bookkeeping

11 Costly Bookkeeping Errors You Can’t Afford to Overlook (and the Quick Fix for Each: A brisk walk through the small-but-mighty mistakes that quietly grow teeth if left alone. Each error comes with a simple, immediate fix so you can stop problems before they snowball into something far harder (and far pricier) to untangle.

Make DIY, Outsourced or Hybrid Bookkeeping Work for Your Business Goals: Thinking of doing it all yourself? Here’s a friendly look at where DIY shines, where it can quietly unravel your finances, and how to know when it’s time to call in a pro — before your spreadsheets start judging you.

Manage Your Side Hustle Taxes Without Losing Your Joy (and Without Overpaying): Whether you’re selling candles, coaching online, or finally monetising your love of crochet, this guide breaks down what you actually need to track for tax time. Clear steps, zero jargon, and no panic required.

© 2026 LiftFin-Confidence. All rights reserved. Privacy Policy | Terms of Service